The 41-Point Gap That Vertical AI Is Built to Close

83% of enterprises deployed AI. 42% of mid-market has. The gap between them is the biggest GTM opportunity in a decade.

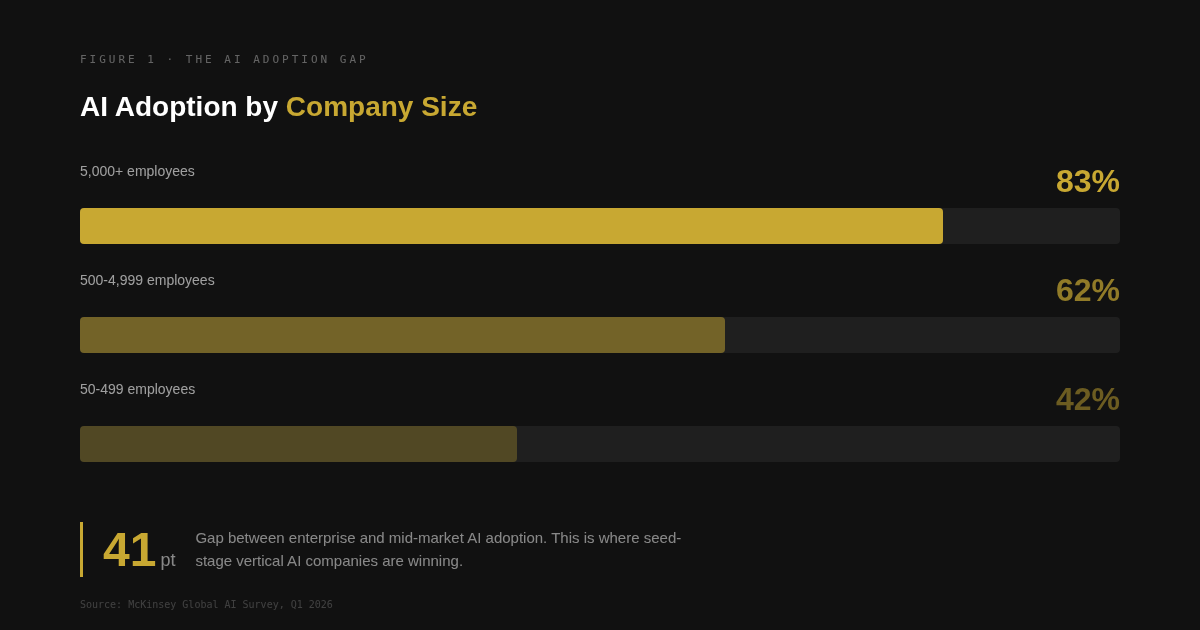

McKinsey’s Q1 2026 Global AI Survey puts the numbers side by side. 83% of companies with 5,000+ employees have deployed AI. 62% of companies with 500 to 4,999 employees. 42% of companies with 50 to 499. The gap between the top and the bottom of that range is 41 percentage points. Most people read that as a technology adoption curve. Enterprises lead, mid-market follows, eventually everyone catches up.

That is the wrong read. The gap is not about readiness. It is about how purchasing decisions get made. Enterprise AI adoption is high because enterprises have dedicated procurement teams, IT departments, and innovation budgets designed to evaluate, pilot, and deploy new technology. Mid-market AI adoption is lower because mid-market companies have none of those things. Not because they do not want AI. Because the way AI has been sold does not match the way they buy.

The 41-point gap is a go-to-market problem. And it is where the fastest-growing category of AI companies is being built.

Where Purchasing Authority Lives

The average B2B enterprise deal now involves 6.8 stakeholders, up from 5.4 in 2020. SOC 2, GDPR, and vendor risk assessments add two to four weeks to the average cycle. Enterprise sales cycles for software above $100K ACV run 90 to 180+ days. Some stretch past twelve months. The cycle has actually gotten longer since 2022, not shorter, as CFO scrutiny and committee buying have intensified.

This is not dysfunction. It is the natural result of how enterprise organizations distribute purchasing authority. Budget authority sits with finance. Technical approval sits with IT. Security approval sits with infosec. Business case approval sits with the executive sponsor. Each node in the chain adds time, and each node optimizes for its own risk function, not for speed.

Mid-market purchasing authority works differently. At a 200-person company, the person who feels the operational pain is often the same person who can approve a $500/month tool. There is no procurement layer between the problem and the purchase. SMB deals with less than $15K ACV close in 14 to 30 days. The constraint is not approval chains. It is whether the product demonstrates value fast enough to justify the spend.

This structural difference in how authority is distributed creates two entirely different sales architectures. Most AI companies only build for one of them.

The Vertical AI Wedge

Horizontal AI tools compete on capability breadth. They serve every industry, every function, every workflow. That generality is an asset in enterprise, where a platform needs to integrate across departments and justify a six-figure purchase to a cross-functional committee. It is a liability in mid-market, where the buyer does not need a platform. They need one problem solved completely.

Vertical AI is a $3.5 billion category as of 2025, triple the investment from the previous year. The growth is not evenly distributed. It is concentrated in companies that pick a specific industry, a specific workflow, and a specific buyer persona, then build a product that works on day one without configuration, integration, or training.

A logistics company with forty trucks does not need a general-purpose optimization platform. It needs a routing tool that accounts for its specific delivery windows, vehicle capacities, and driver schedules. A dental practice group does not need an enterprise analytics suite. It needs a system that reads patient no-show patterns and adjusts scheduling automatically. The narrower the product, the faster the buyer sees value. The faster they see value, the shorter the sales cycle.

The OECD reported that 91% of SMEs using generative AI report efficiency gains and 76% cite increased innovation. The demand is not missing. The delivery mechanism is. Mid-market companies are not waiting for better models. They are waiting for products that fit into their operating rhythm without requiring an IT department to deploy them.

Revenue Velocity, Not Revenue Size

The math on mid-market vertical AI breaks the assumptions that enterprise SaaS trained into an entire generation of founders and VPs of Sales.

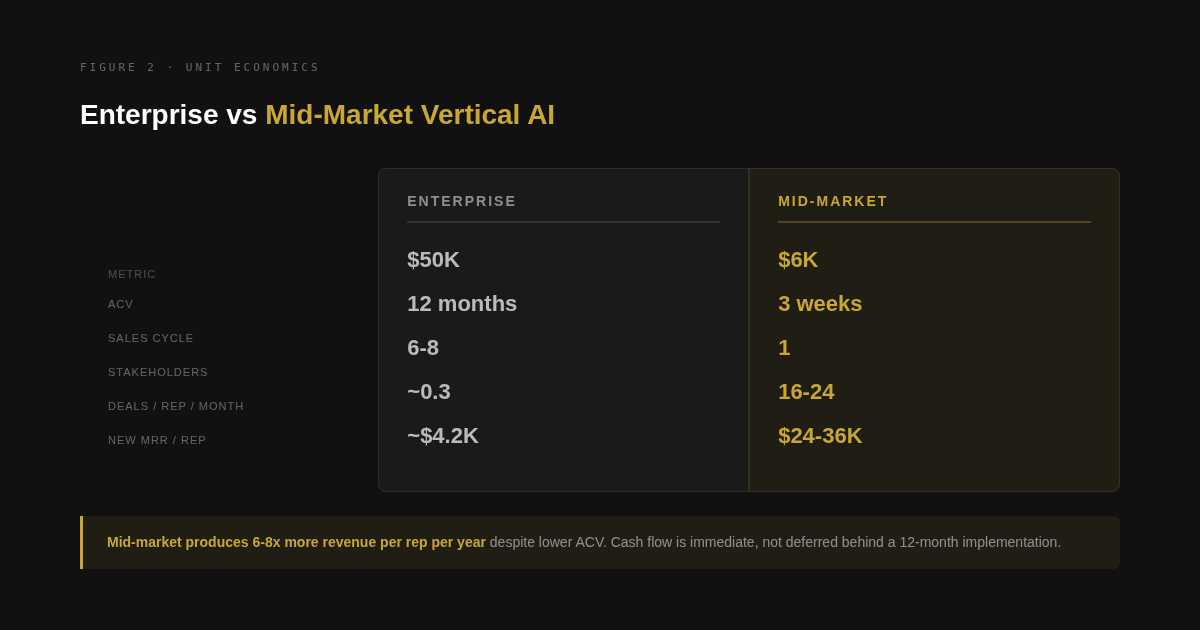

Enterprise logic: optimize for average contract value. A $50K ACV deal closed once per quarter per rep, after six to twelve months of cycles, produces $200K in annual revenue per rep. The number looks clean on a board deck.

Mid-market vertical AI logic: optimize for deal velocity. A $6K ACV product ($500/month) closed in two to three weeks means a single rep can close 16 to 24 deals per month. That is $96K to $144K in new ARR per month from one person. Revenue per rep per year is not even close.

The cash flow dynamics are equally different. Enterprise revenue is deferred behind pilots, implementation timelines, and net-60 payment terms. Mid-market revenue arrives the week the customer signs up. Credit card on file. No invoice. No accounts receivable aging. For a seed-stage company trying to hit $1M ARR, the difference between collecting revenue in week three versus month twelve is the difference between surviving and running out of runway.

AI pilot-to-contract conversion rates reinforce this. 47% of AI pilots convert to paid contracts, compared to roughly 25% for traditional software. The product either works or it does not. Mid-market buyers do not run six-month evaluations. They run the tool for a week. If it solves the problem, they pay. If it does not, they leave. The binary nature of the decision compresses the entire evaluation cycle into days.

The GTM Architecture That Fits

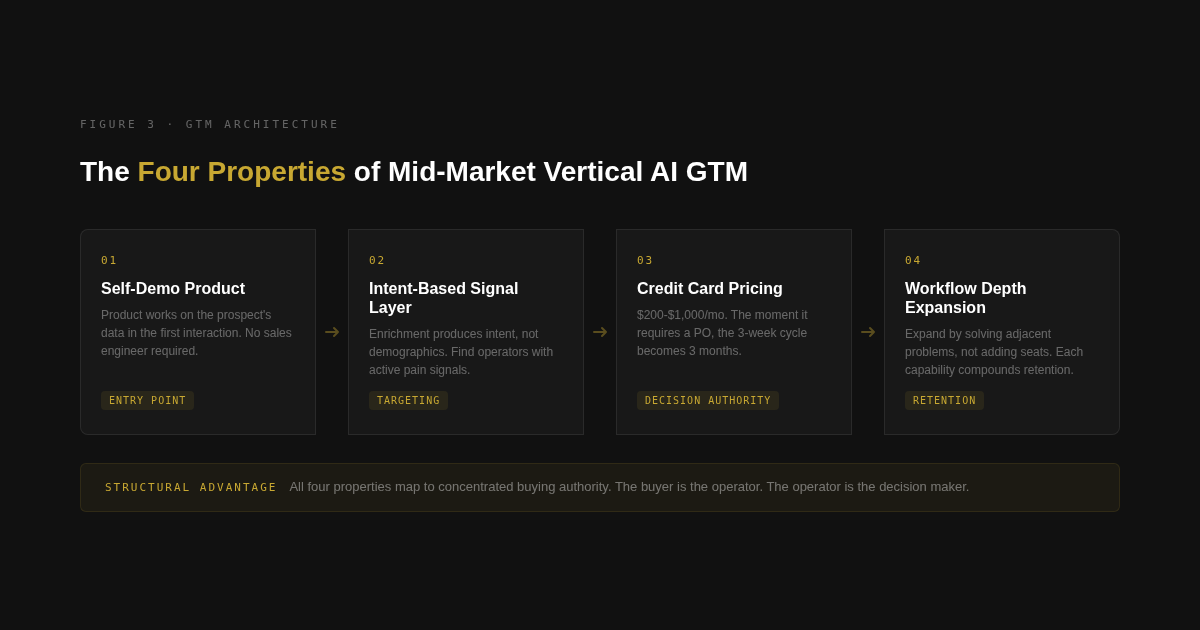

Selling into the 41-point gap requires building a go-to-market system around how mid-market actually buys. The architecture has four structural properties, and each one maps back to the same root cause: purchasing authority is concentrated, not distributed.

First, the product must demonstrate value without human intervention. Mid-market buyers do not book discovery calls as a first step. They want to see the product work on their problem before they talk to anyone. Self-serve trials, instant demos with the buyer’s own data, or free tiers that expose the core value proposition are the entry point. If the first interaction requires a sales engineer, the architecture is wrong for this segment.

Second, the signal layer must produce intent, not firmographics. The 50% of SMEs that report lacking AI skills are not going to respond to a cold email about “AI-powered solutions.” The signal that matters is operational: a founder posted about a specific workflow bottleneck, a head of ops searched for a tool to solve a specific problem, a company left a negative review about their current vendor. The enrichment pipeline must surface people who are actively experiencing the pain the product solves.

Third, pricing must sit below the purchase order threshold. The moment a product costs more than what an operator can put on a corporate card, a procurement process activates. At most mid-market companies, that threshold is somewhere between $1,000 and $2,500 per month. Below it, the operator decides. Above it, finance gets involved, the cycle extends, and the structural speed advantage disappears. Pricing is not a revenue decision. It is an architecture decision that determines which buying motion the product triggers.

Fourth, expansion is vertical, not horizontal. Enterprise SaaS expands by adding seats across departments. Mid-market vertical AI expands by solving adjacent problems for the same buyer. The restaurant review monitoring tool adds menu optimization. The logistics routing tool adds demand forecasting. The dental scheduling tool adds patient communication. Each new capability deepens the workflow integration, increases switching costs, and grows contract value without a new sales cycle. Expansion revenue from self-serve (upsells, add-ons, higher tiers without sales intervention) is the metric that signals this architecture is working.

The Two Failure Modes

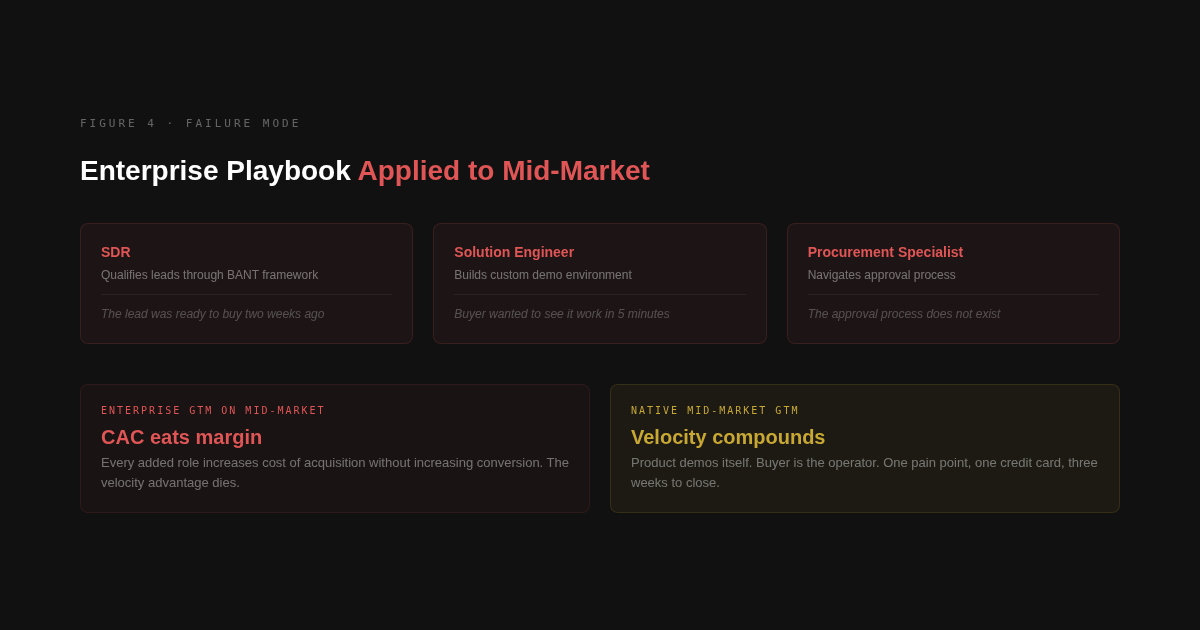

The first failure mode is applying enterprise GTM to a mid-market product. A vertical AI company raises a Series A, hires a VP of Sales from a company that sold $100K ACV deals, and builds a team designed for long cycles. SDRs qualify leads through discovery frameworks that take two weeks. Solution engineers build custom demos for buyers who wanted to see the product work in five minutes. The company layers roles designed for distributed purchasing authority onto a segment where authority is concentrated. Each added headcount increases cost of acquisition without increasing conversion. The velocity advantage that made the product work at seed stage gets buried under enterprise overhead.

The second failure mode is trying to move upmarket without rebuilding the GTM architecture. A vertical AI company that closes $500/month deals with a product-led motion tries to land $50,000/year enterprise contracts with the same approach. The self-serve trial that converted operators does not convert procurement committees. The pricing page that let buyers swipe a card does not satisfy an enterprise vendor evaluation. Moving upmarket is not a pricing change. It is a full rebuild of the signal layer, the sales motion, the pricing model, the security posture, and the expansion strategy. Companies that try to stretch one GTM architecture across both segments end up competitive in neither.

The Structural Implication

The 41-point gap will not close by mid-market companies slowly adopting enterprise AI tools. It will close because a new generation of vertical AI companies is building products and GTM motions designed specifically for how mid-market buys. The OECD data shows SME AI adoption growing 72% year over year. The McKinsey data shows the gap still wide. The companies that close it will not be the ones with the best models. They will be the ones whose go-to-market architecture matches the purchasing architecture of the buyer.

For founders: pick the vertical where the operator is the buyer. Build a product that demonstrates value in the first session. Price it within credit card authority. Build enrichment that surfaces intent signals, not company lists. Run the motion at velocity. Expand through workflow depth. The 41-point gap is not a problem waiting for a technology solution. It is a market waiting for the right GTM architecture.

Sources: McKinsey Global AI Survey Q1 2026, OECD AI Adoption by SMEs 2025, Techaisle SMB AI Adoption Trends 2025