You're Building the Wrong Moat

AI collapsed the cost of copying your product and the moat moved to distribution before most GTM teams noticed

👋 Hi, it’s Rick Koleta. Welcome to GTM Vault - a breakdown of how high-growth companies design, test, and scale revenue architecture. Join 26,000+ operators building GTM systems that compound.

The product is no longer the moat. For most founders reading this, that sentence either lands as obvious or alarming. If it feels obvious, the question is whether your GTM motion reflects it. If it feels alarming, this piece is for you.

Every era of B2B software is defined by a single binding constraint. The companies that win each era are not necessarily the ones with the best product. They are the ones that identify what the binding constraint is, build their entire motion around collapsing it, and move before the previous generation realizes the game changed.

The constraint that defined the last decade was building. Shipping enterprise-grade software required two to four years of runway, ten to thirty engineers, and infrastructure spend that only institutional capital could absorb. The product was hard to copy, so the moat lived inside it.

AI collapsed that constraint. The cost to build is approaching zero. The cost to copy is even lower. A category leader that once had six months to compound a product advantage before a well-funded competitor matched it now has weeks. The product is still necessary. It is no longer sufficient.

The moat moved. It is sitting in distribution now.

The Historical Record

The relationship between distribution and product outcome is not new. It shows up across the last fifteen years of B2B software in the same pattern: the company that builds the audience first wins, even when it has the weaker product. The examples closest to this audience make the point most clearly.

ZoomInfo had the deeper data asset, the larger enterprise contracts, and the sales machine to match. Apollo entered the market with a thinner database and a fraction of the budget. What Apollo had was distribution: a freemium motion that put the product directly in the hands of SDRs and revenue operators who couldn’t afford ZoomInfo’s six-figure contracts. Those users became evangelists. They brought Apollo into new companies when they changed jobs. They built sequences, shared templates, and talked about it in Slack communities that ZoomInfo’s field team had never set foot in. Apollo reached a $1.6 billion valuation not by out-featuring ZoomInfo but by owning the distribution layer ZoomInfo had ignored.

Gong did not win the conversation intelligence category by building a better recorder. Clari, Chorus, and a half-dozen other tools were competing on features at the same time. Gong won by creating the category itself. The “revenue intelligence” framing, the state of remote selling reports, the relentless content engine that owned every search term a revenue leader would type on a bad pipeline quarter. By the time enterprise buyers were ready to evaluate, Gong was already the default answer. Chorus sold to ZoomInfo for $575 million. Gong’s last valuation was $7.25 billion.

Clay became the operating system for GTM engineers before most companies knew what a GTM engineer was. The product was technically sophisticated and genuinely hard to copy. But the moat was not the product. It was the community of operators who had built their entire outbound infrastructure on Clay, documented it publicly, and evangelized it in every GTM Slack, newsletter, and conference session they could find. When competitors with similar feature sets entered the market, they were not competing against Clay’s product. They were competing against Clay’s distribution, which had already saturated the audience that mattered.

What is different now is not the pattern. It is the stakes. In each of those examples, distribution beating product was still somewhat exceptional, the result of a founder who saw an angle. In the current era, it is the only durable path. The window to build a product moat is gone. Distribution is what remains.

If you want to see distribution-first operators break down the exact systems they built, that's Show Me Your Stack. Every episode is here.

The Sequence Changed

Founders have been given the same playbook for two decades. Build the product. Find product-market fit. Then figure out go-to-market.

That sequence was designed for a world where the product was hard to copy and distribution was something you bolted on after you had proof. That world is gone.

Go-to-market is not what you do after product-market fit. It is how you get product-market fit. The audience you build before launch is the population you test with. The trust you earn before the product is finished is the credibility that converts skeptics into early customers. The brand you establish in a category before anyone else arrives is the default that compounds for years after the market matures.

Ironclad became the default contract lifecycle management platform for in-house legal teams before its product could match what DocuSign or legacy CLM tools offered on paper. The feature gap was real. The distribution gap was larger. Ironclad showed up inside legal operations communities, built trust with general counsels before they had budget to evaluate vendors, and established the category name before the category had a formal RFP process. By the time procurement got involved, the decision was already made. Replit ran the same play with a different audience. It built distribution through students and early-career developers who had no purchasing authority. When those developers moved into engineering roles at companies with real budgets, they did not run a vendor evaluation. They installed what they already trusted. Replit’s enterprise motion did not start with enterprise sales. It started with a free tier that its competitors dismissed as a hobbyist product.

The founders who deferred distribution are learning this at Series A, when a competitor with a comparable product and an established audience is converting faster without a better product. By then, catching up costs more than starting right would have.

The Benchmarks Confirm It

The pace at which this is playing out is structurally different from any previous software cycle.

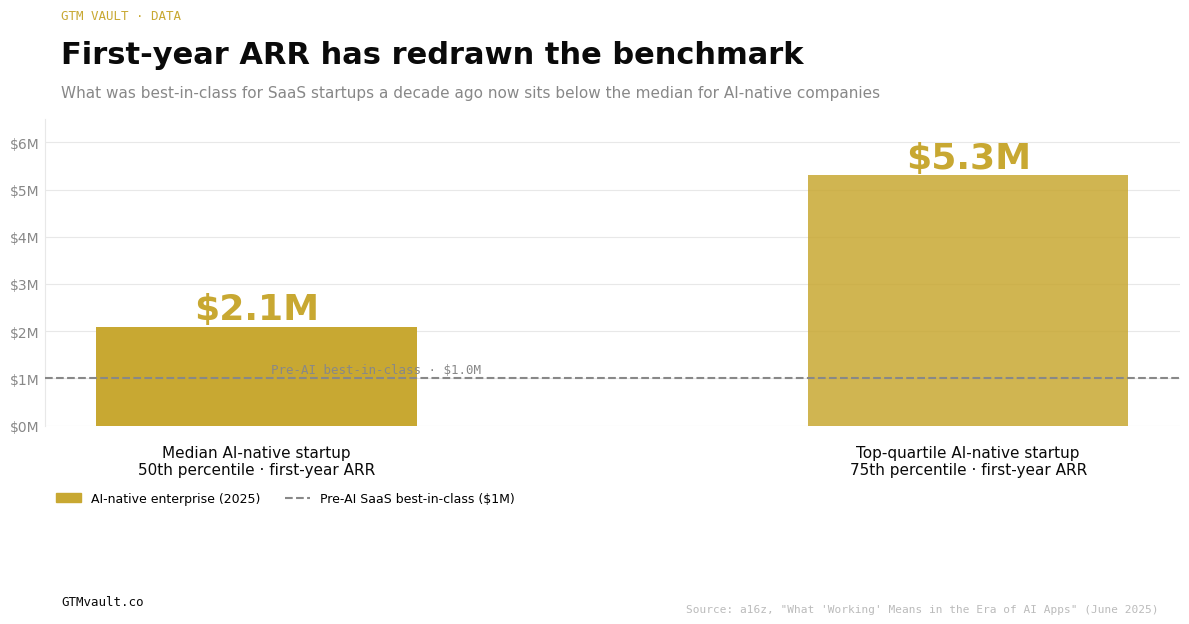

Source: a16z, “What ‘Working’ Means in the Era of AI Apps” (June 2025)

The median enterprise AI startup reaches $2.1 million ARR by month twelve. The top quartile reaches $5.3 million. What was best-in-class for SaaS companies a decade ago, $1 million ARR in year one, now sits below the median for AI-native companies. Series A rounds are happening at nine months post-revenue.

Markets are getting called earlier, with less data and higher conviction, because the investors who wait for traditional proof points are being priced out. The companies that establish default-brand status in a new category before the market decides do not need to maintain it aggressively. They need to establish it once. After that, the compounding does the work.

The implication for founders is not that they should move faster on product. They should move faster on audience. The window between category creation and category lockout is compressing in direct proportion to how fast the product can be copied.

The Anthropic Signal

The fastest-growing software company in history is concentrating its hiring around how to sell, not just how to build.

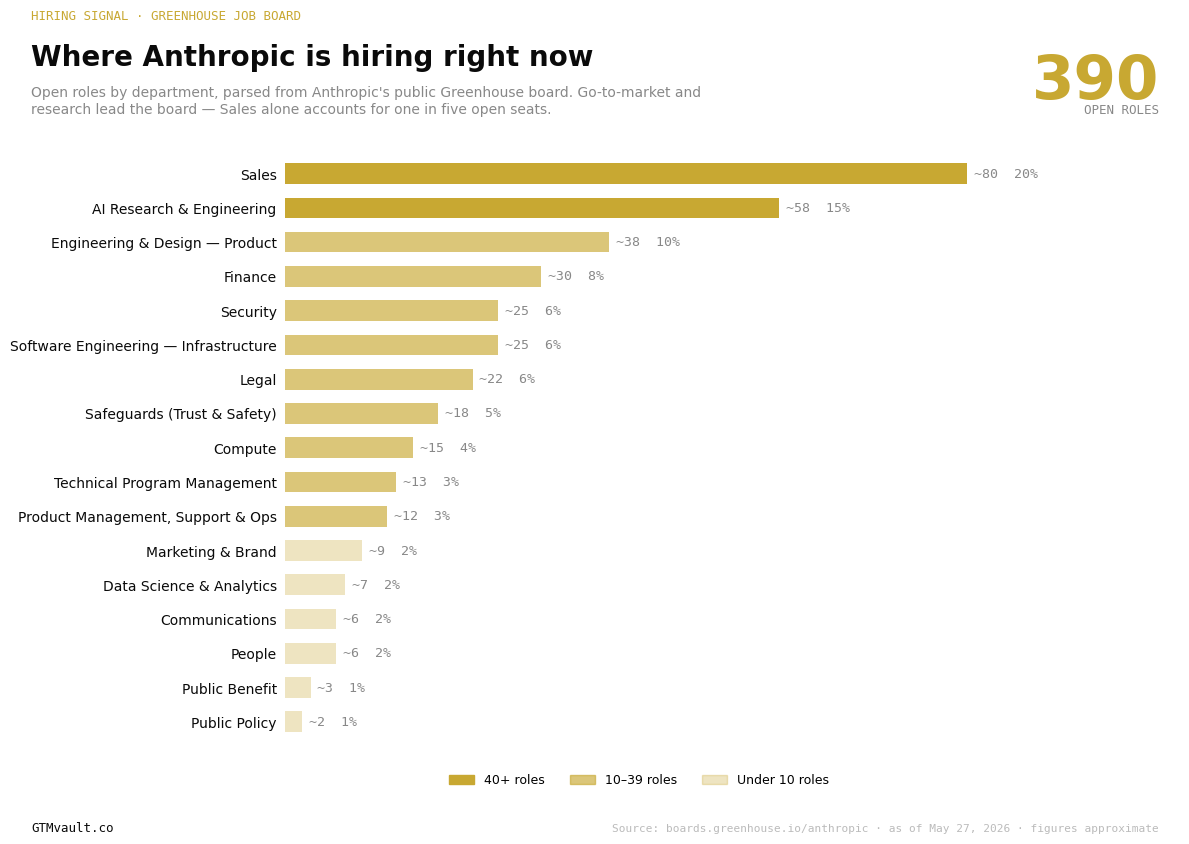

Source: boards.greenhouse.io/anthropic · as of May 27, 2026 · figures approximate

Sales is Anthropic’s single largest open department. It accounts for one in five open roles, ahead of AI research, product engineering, and every other function. The company with arguably the strongest model position in the world is betting more on distribution than on product right now.

This is not a coincidence. It is the logical conclusion of the constraint shift. When the product can be matched, the durable advantage lives in the relationships, the brand presence, and the market access that a well-built GTM motion produces. Anthropic knows this. The companies that survive the next decade will build accordingly.

Distribution Is a System, Not a Channel

The mistake most founders make when they accept the distribution-first thesis is treating distribution as a single channel decision. They pick LinkedIn, or a podcast, or a newsletter, and optimize it in isolation. That is not distribution. That is a channel experiment.

Distribution is a system with inputs, outputs, and feedback loops. The audience you build in one channel becomes the distribution mechanism for every channel that follows. The trust you earn through one piece of content becomes the conversion layer for the next product you ship. The ICP you identify through early distribution informs the product roadmap that deepens the moat.

The founders winning the Distribution Era are not the ones with the largest followings. They are the ones who built the tightest feedback loop between distribution and product, so that audience growth and product-market fit converge instead of developing in parallel.

That convergence is the compound return that distribution provides when it is treated as a system. A channel is a tactic. A distribution system is what makes the next product launch, the next category expansion, and the next pricing increase easier than the last one. The audience you built absorbs each of them before the market has time to generate friction.

The Structural Implication for GTM Teams

If you are running GTM at a company where distribution is still treated as a downstream activity, the constraint is not budget or headcount. It is sequencing.

The GTM teams that are winning are not running larger programs. They are running earlier ones. They are building the audience before the product is finished, establishing the brand before the category is defined, and converting the trust they earned in distribution into pipeline at a rate that outbound programs cannot match on a comparable cost basis.

The product still has to be exceptional. That requirement did not change. The order changed. Build the audience first. Ship the product into a market that already believes in you.

The moat is not inside the product anymore. It is in the relationship between the product and the people who were already waiting for it.